Disclaimer: This article is for educational purposes only and does not constitute financial advice. Please consult a qualified financial planner for your specific situation.

Living paycheck to paycheck is exhausting. You might feel like you make enough money, yet at the end of the month, your bank account is hovering near zero. The problem usually isn’t how much you make; it’s how you allocate it.

Finding the right budget percentage breakdown is the secret weapon of personal finance. Instead of obsessing over every penny, you assign your income to broad categories. This simplifies your life and ensures your bills, fun, and future are all covered.

Here is how to structure your income for financial freedom.

Contents

The Gold Standard: The 50/30/20 Rule

Popularized by Senator Elizabeth Warren, this is the most effective starting point for 90% of people. It balances responsibility with enjoyment so you don’t burn out.

The concept is simple: you divide your after-tax income (what actually hits your bank account) into three buckets.

1. 50% for Needs (The “Must-Haves”)

These are the bills you absolutely cannot avoid. If you lost your job tomorrow, these are the expenses that would still exist.

-

Rent/Mortgage: Ideally, this should not exceed 30% of your income alone.

-

Utilities: Electricity, water, internet, and phone.

-

Groceries: Basic food to eat at home (not dining out).

-

Transportation: Car payments, gas, insurance, or public transit passes.

-

Minimum Debt Payments: The minimum due on credit cards or loans to avoid default.

If your needs are over 50%: You have an income problem or a lifestyle problem. You may need to downsize your apartment, trade in a car, or pick up a side hustle to bring this number down.

2. 30% for Wants (The “Nice-to-Haves”)

This is the category that makes life worth living. It is the first to be cut if you lose income, but it is essential for your mental health.

-

Dining Out & Bars: Friday night pizza, drinks with friends.

-

Entertainment: Netflix, Spotify, concert tickets, video games.

-

Shopping: New clothes, gadgets, or home decor.

-

Travel: Weekend getaways or saving for a big vacation.

Why 30%? It sounds high, but restricting this category too much leads to “frugal fatigue,” where you snap and binge-spend. Giving yourself permission to spend 30% guilt-free helps you stick to the plan long-term.

3. 20% for Savings & Debt (The “Future You”)

This is the wealth-building bucket. This money is “gone” as soon as you get paid—moved to a separate account or used to destroy debt.

-

Emergency Fund: Building 3-6 months of expenses.

-

Retirement: 401(k) or IRA contributions.

-

Extra Debt Payments: Anything above the minimum payment to pay off loans faster.

-

Big Goals: Saving for a down payment on a house or a wedding.

Alternative Breakdowns

The 50/30/20 rule isn’t a law of physics. Depending on your life stage, a different budget percentage breakdown might work better.

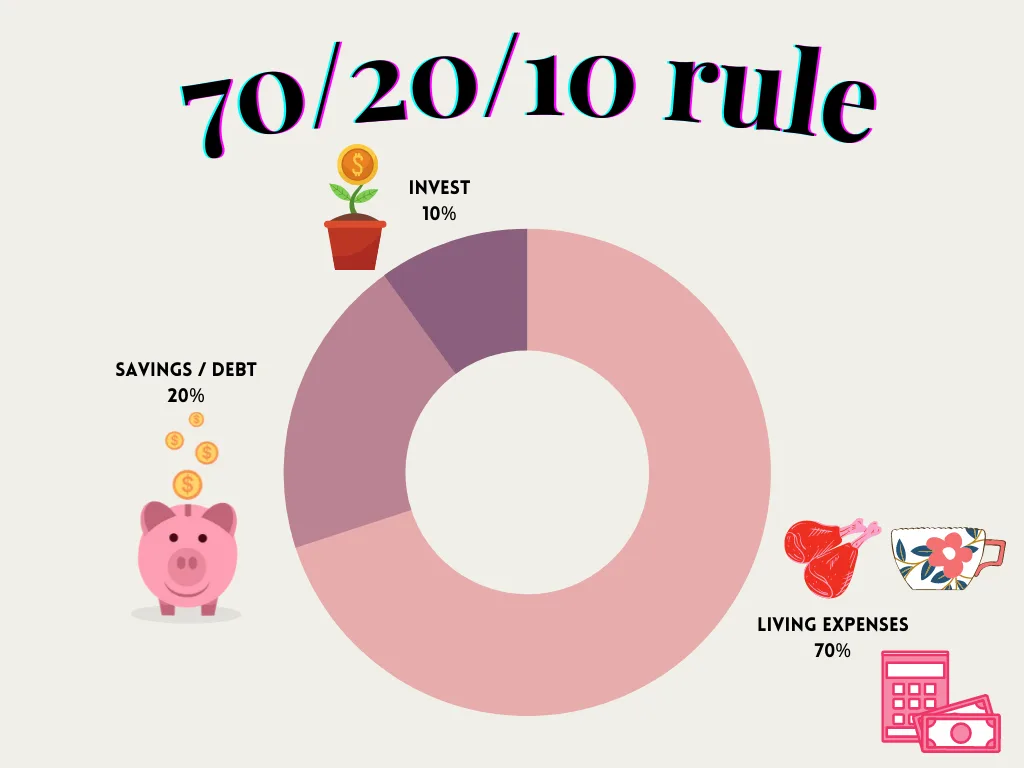

The 70/20/10 Rule (For Tight Budgets)

If you live in a high-cost city or have a lower income, 50% for needs might be impossible.

-

70% Needs: Acknowledges high rent or living costs.

-

20% Savings: Prioritizes debt and safety nets.

-

10% Wants: Sacrifices immediate fun for stability.

The 80/20 Rule (The Minimalist)

If you hate tracking categories, this is for you.

-

20% Savings: Take 20% of your paycheck off the top immediately.

-

80% Everything Else: Spend the rest however you want. As long as the savings are safe, the details don’t matter.

Real World Example: Salary of $4,000/Month

Let’s see how a typical budget percentage breakdown looks for someone bringing home $4,000 a month after taxes.

| Category | Percentage | Amount | Where it goes |

|---|---|---|---|

| Needs | 50% | $2,000 | Rent ($1,200), Car/Transit ($400), Groceries ($300), Utilities ($100) |

| Wants | 30% | $1,200 | Restaurants, Netflix, Gym, Hobbies, Clothes |

| Savings | 20% | $800 | Student Loans ($400), Roth IRA ($200), Emergency Fund ($200) |

Final Thoughts

The perfect budget isn’t the one that looks best on a spreadsheet; it’s the one you can actually stick to. Start with the 50/30/20 breakdown. If your “Needs” are too high, don’t panic—just aim to adjust your percentages by 1% or 2% each month until you find balance.